"Buy" Signals Are Adding Up

"Buy" Signals Are Adding Up

as uncomfortable as that may make you feel

Boy, was Walter Deemer right. “When the time comes to buy, you won’t want to”.

I really don’t want to start buying the S&P500 a few months before a widely-expected recession — as recessions are typically market killers. Also, the market never bottoms before a recession. Not to mention the often-heard argument, “people will come to their senses as soon as earnings compress the price/earning ratio”...

But the fact of the situation seems to be, folks are convinced that this will be a very weak and short recession, the famous ‘soft landing’, which the markets will be able to shrug off.

Or, investors are thinking: yes, there will be a recession, but then interest rates will go down, causing the stock market to become bullish — so let’s get in early!

Difficult times! But in the end, it’s important to remember we’re not trying to be smarter than other people; we just want to make money. And that “price” (i.e., the stock market) creates its own reality. So let’s see what it’s telling us.

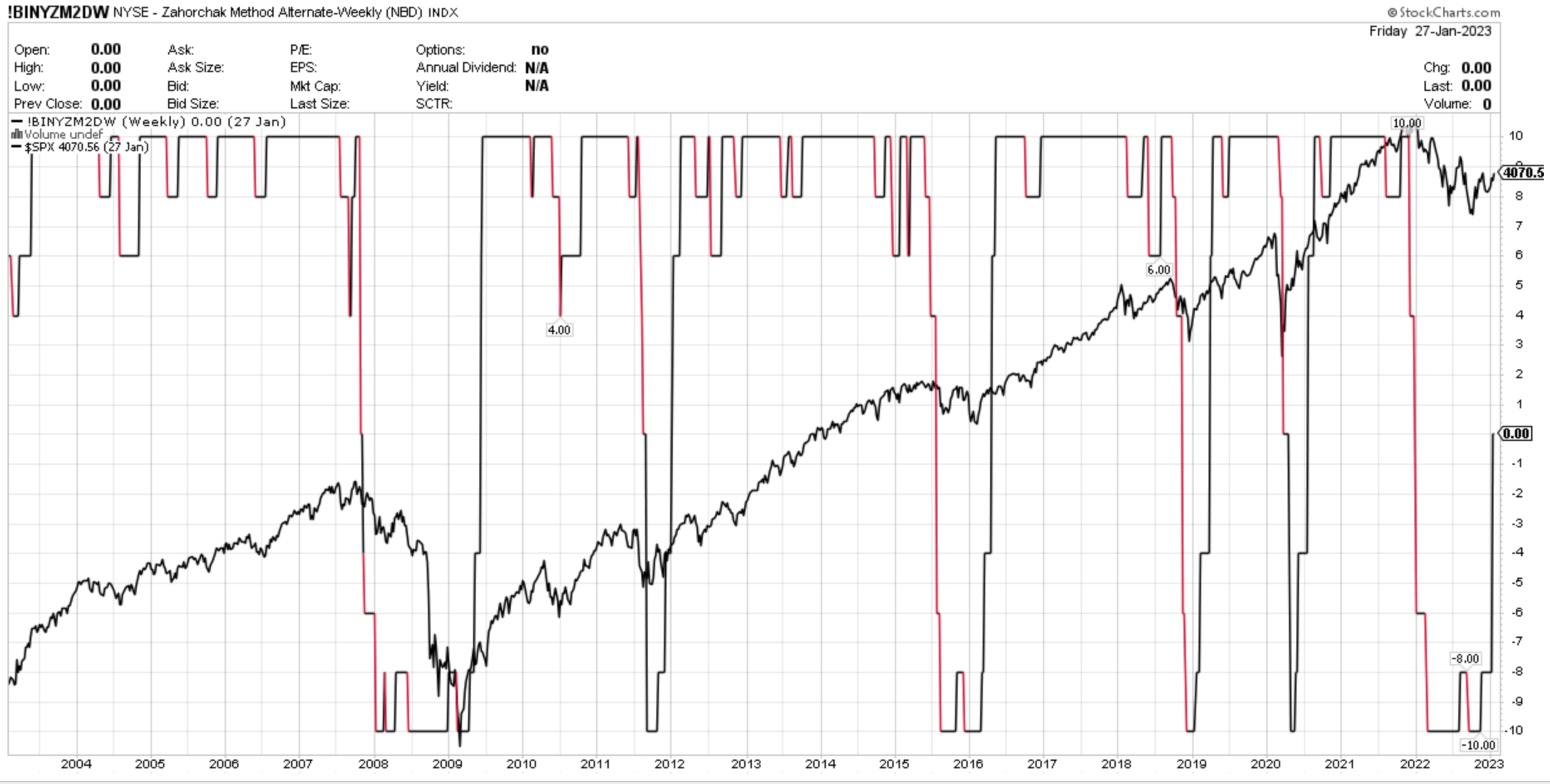

The Zahorchak signal is marching up to a “ten” level, at which it would clearly signal risk-on.

Looking back 40 years, there have been only two instances in which it didn’t follow through from its present level of “zero”: in 1982, and in 1990. If the market doesn’t soon reverse in a hard way, Zaharchak will be a very green light quite soon. Subscribe, and I’ll keep you posted!

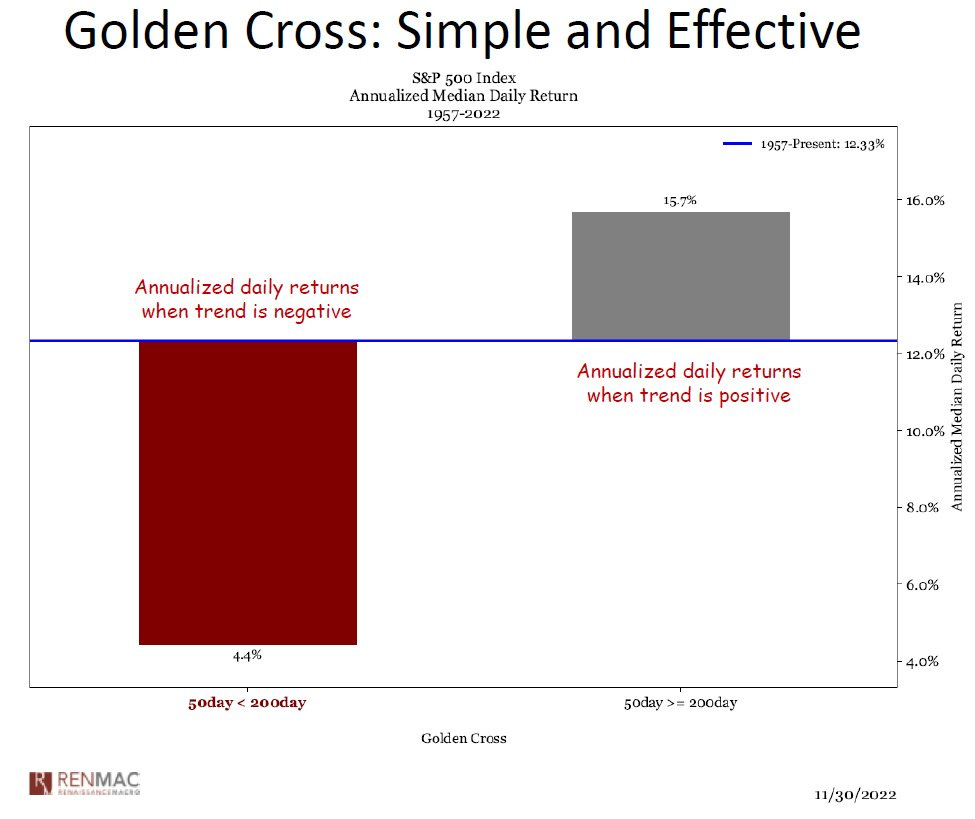

The S&P 500 is now in Golden Cross territory.

Respect the Golden Cross!

Two and a half weeks ago, Mark Ungewitter commented on the Percent Price Oscillator...

Back then, the PPO was at around -2.5%; yesterday its level reached +0.391%, a lot closer to the +2.5% target. Again, it seems we’re getting there!

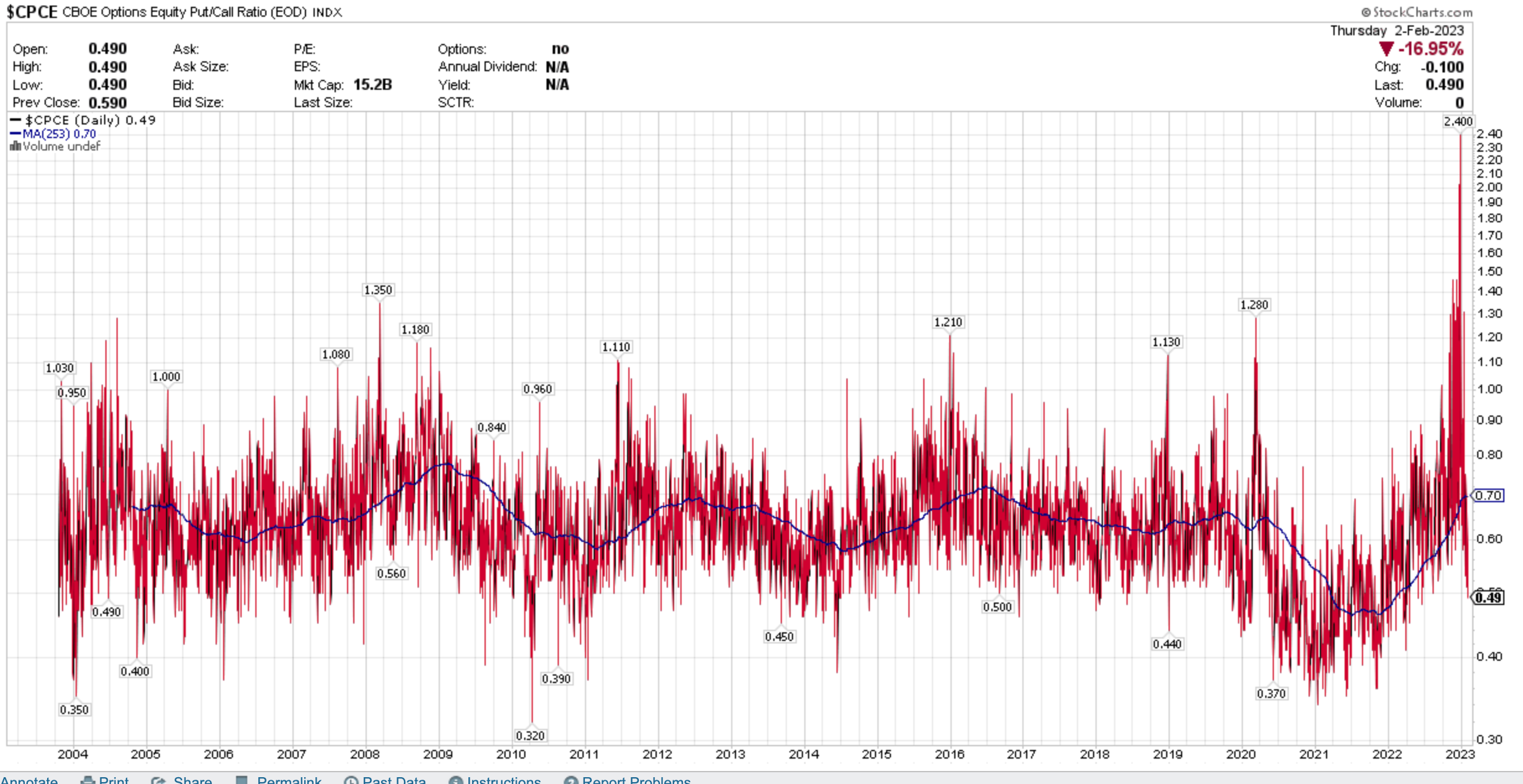

Long-term readers will have noticed I like a certain Long-Term Sentiment metric. And this is recently looking much better, too.

The ratio of put-to-call options indicated a record-breaking level of fear in December 2022, but has recently gone much lower. And after a year of negative sentiment, its long-term moving average has reached a level at which previous market turnarounds have taken place.

I am not too worried about the Baltic Dry Index’s miserable-looking chart. This may well have to do with newly-available shipping capacity in China.

So, there we go. I had a lot of good reasons to not call a final October low, and to not participate in this January’s bull run: most charts just weren’t adding up.

That said, in late October, I recommended looking at the Polish stock market as a light-at-the-end-of-the-tunnel indicator of global risk: if it continued to be positive, the worst could be over. It did, and it was! (Or at least, that’s how it seems to be).

Anyway, by now the sum of the evidence is making the Bear case more and more difficult to advocate. Therefore, I have started to nibble in and will take some more bites as conditions further improve.

What about you? Are you a perma-skeptic, or are you hoping for a proper crash, or are you an opportunist, like me? Let me know in the comments, please!

Martin, thanks for updates on the signals you follow!

Regarding your statement, "I really don’t want to start buying the S&P500" -- there are a lot of alternatives to buying the S&P 500, starting with your observation that annual return rankings often reverse year to year.

I mentioned your idea on Cliff's blog, and another commenter ran the numbers and found that buying last year's three worst performing sectors (excluding energy) beat the S&P over the period covered by the chart from NovelInvestor.com:

https://cliff-smith-blog.freeforums.net/post/1307/thread

"And that “price” (i.e., the stock market) creates its own reality." No kidding!