We're Not There Yet

We're Not There Yet

Just a few lights at the end of this bear market's tunnel

One of the disagreeable things about a bear market is how it makes you feel like you’re nine years old again, sitting in the back of your parent’s car, during a road trip.

“Are we there yet?” “No honey, we just started driving fifteen minutes ago.”

You feel constant discomfort, sometimes even nausea (back in the day, cars pitched and wallowed, and adults smoked), and you spend what feels like years wishing it was just over.

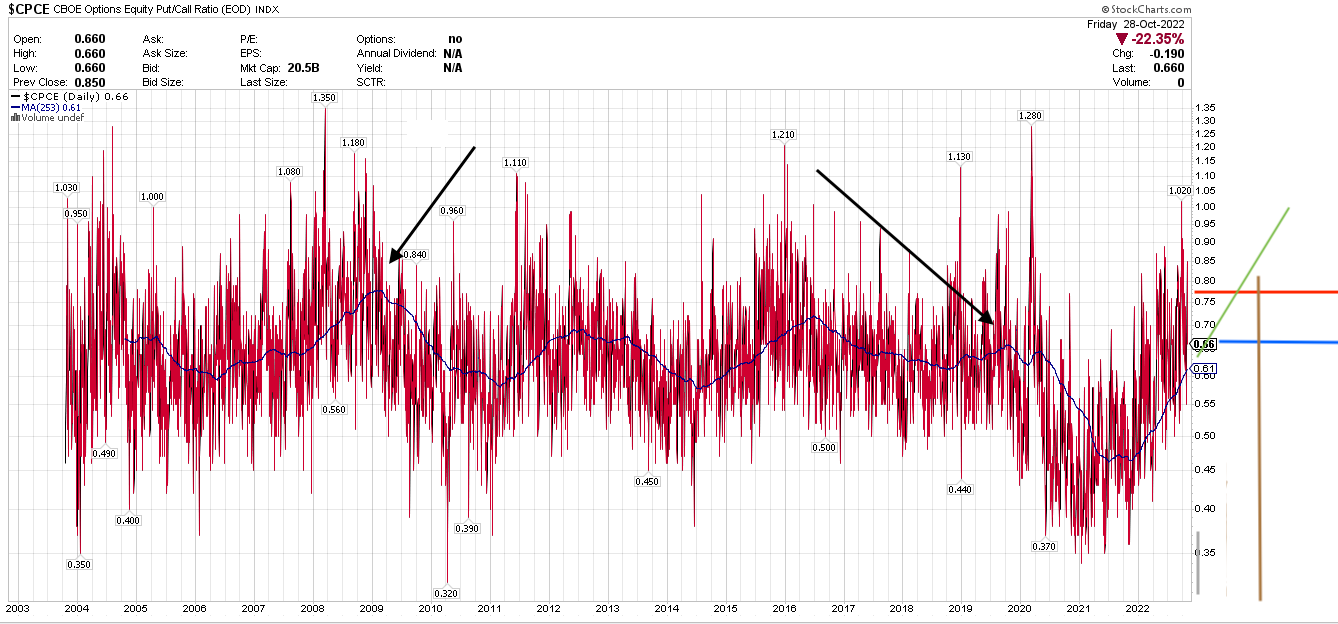

Moving on from sweet youth to the stock market: back in March 2022, I wrote about the phenomenon of long-term moving averages of sentiment. My hypothesis was that the irrational exuberance which is typical for a bull market does not just go away after a few underperforming weeks.

It takes months, sometimes years of a miserable stock market to wash out all the shaky hands, to force people who had previously refused to give up hope… to finally sell.

Markets bottom not because of smart buyers, but because the last seller has sold. After which, there are more people buying than there are people selling. Which leads to a new bull.

I was a bit optimistic in March, saying I expected the bear to be over by perhaps November. But please take a look at this updated chart:

I extended the current trend with the green line.

In 2019, the tidal turn from bear to bull (right arrow) happened at the level of the blue horizontal line). If the current trend turns at this level, then this will happen around Q2/2023.

(Note that the grey vertical line corresponds to January 2023, while the brown vertical line is set to January 2024).

In 2008 however, negative sentiment was stronger and went on longer, and the tide didn’t turn (left arrow) before it reached the level indicated by the red horizontal line.

Should the current bear market (in terms of sentiment) resemble 2008, then it won’t be over until around the last quarter of 2023.

Now, none of this is set in stone. The war could end suddenly. Or it, on the other hand, might turn nuclear. The Fed might manage a soft landing… or a pretty uncomfortable global recession might be in store.

Bad news might be good news (a quicker sentiment wash-out). Or, good news could prolong the suffering (more weak hands holding on to stocks for longer).

But wait — this bear market might well continue until Q4/2023?! Aaargh!

As the Bible says, good things come to those who can wait. The opportunity to buy stocks at a generational low such as we had in 2009 would likely be wonderfully profitable — maybe a once-in-an-investor’s-lifetime chance. Keep your powder dry!

Some more charts that might tell us where we stand.

The S&P500 is solidly in black-cross territory, with moving averages slanting downwards.

The Baltic Dry Index is in a firm downtrend, yet nowhere near historic lows. Plenty of room for more bad news here.

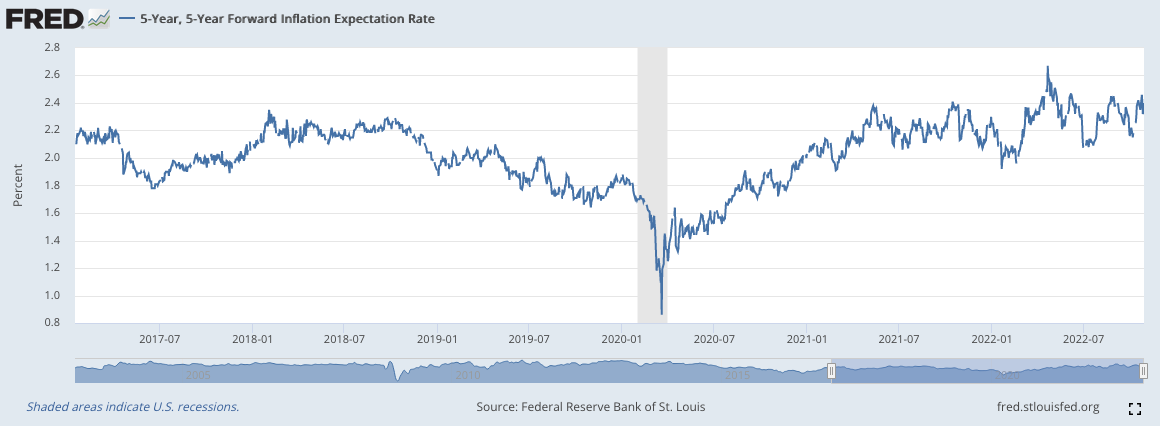

Inflation expectations aren’t particularly low.

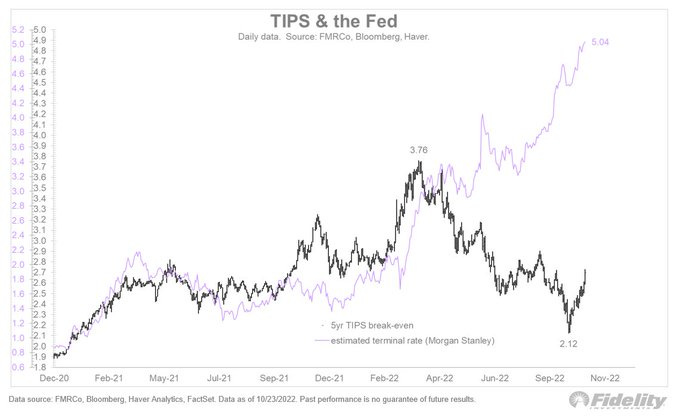

Is all the news bad?

If you look carefully, you might see some light. TIPS (inflation-protected bonds) are behaving strangely, and seem to indicate that inflation has topped.

First out, first in!

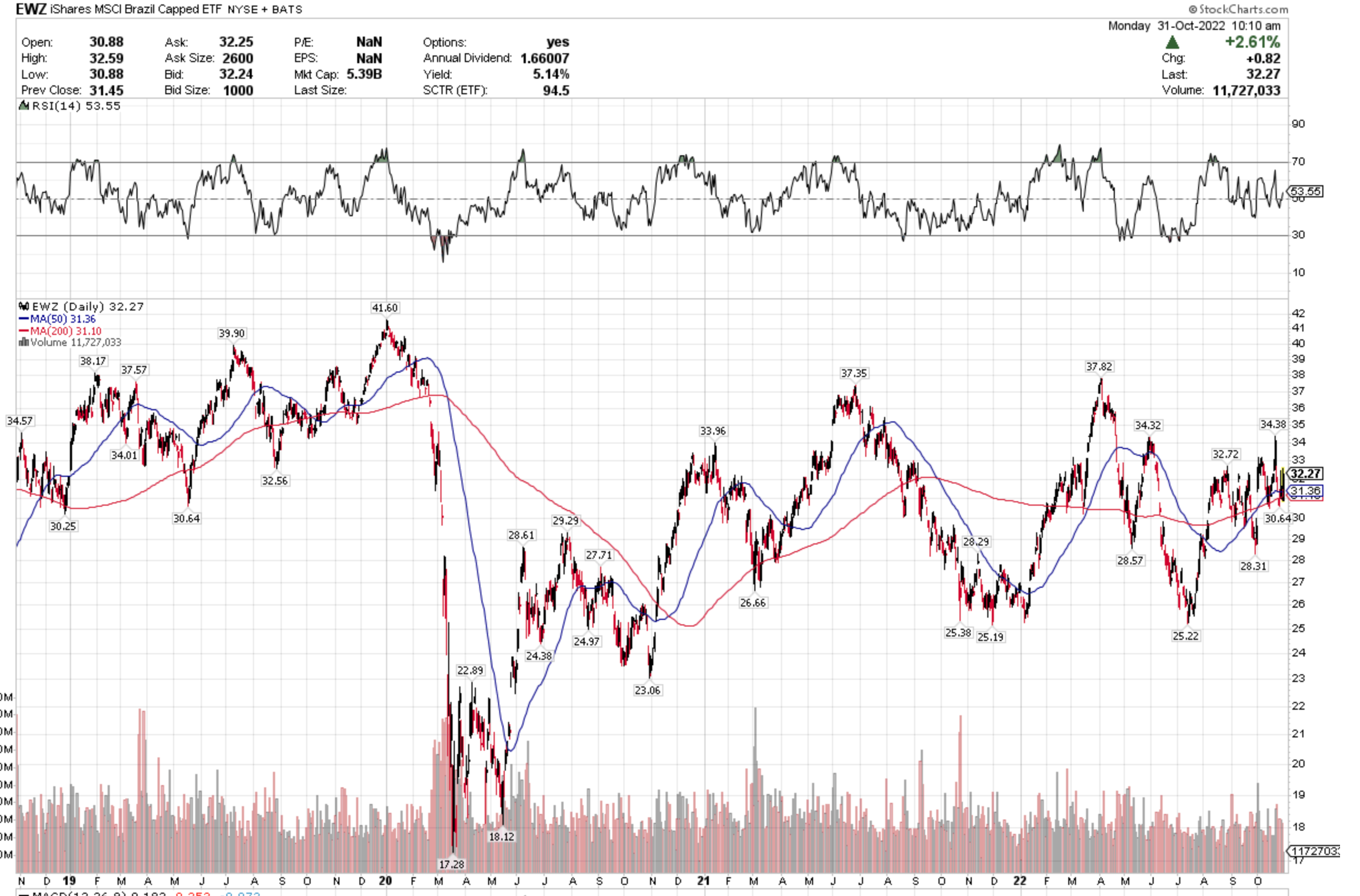

On another positive note, I’d ask you to look away from the U.S. stock market: why wait until (possibly) end-2023 for domestic stocks to bottom, if there’s a bull somewhere else?

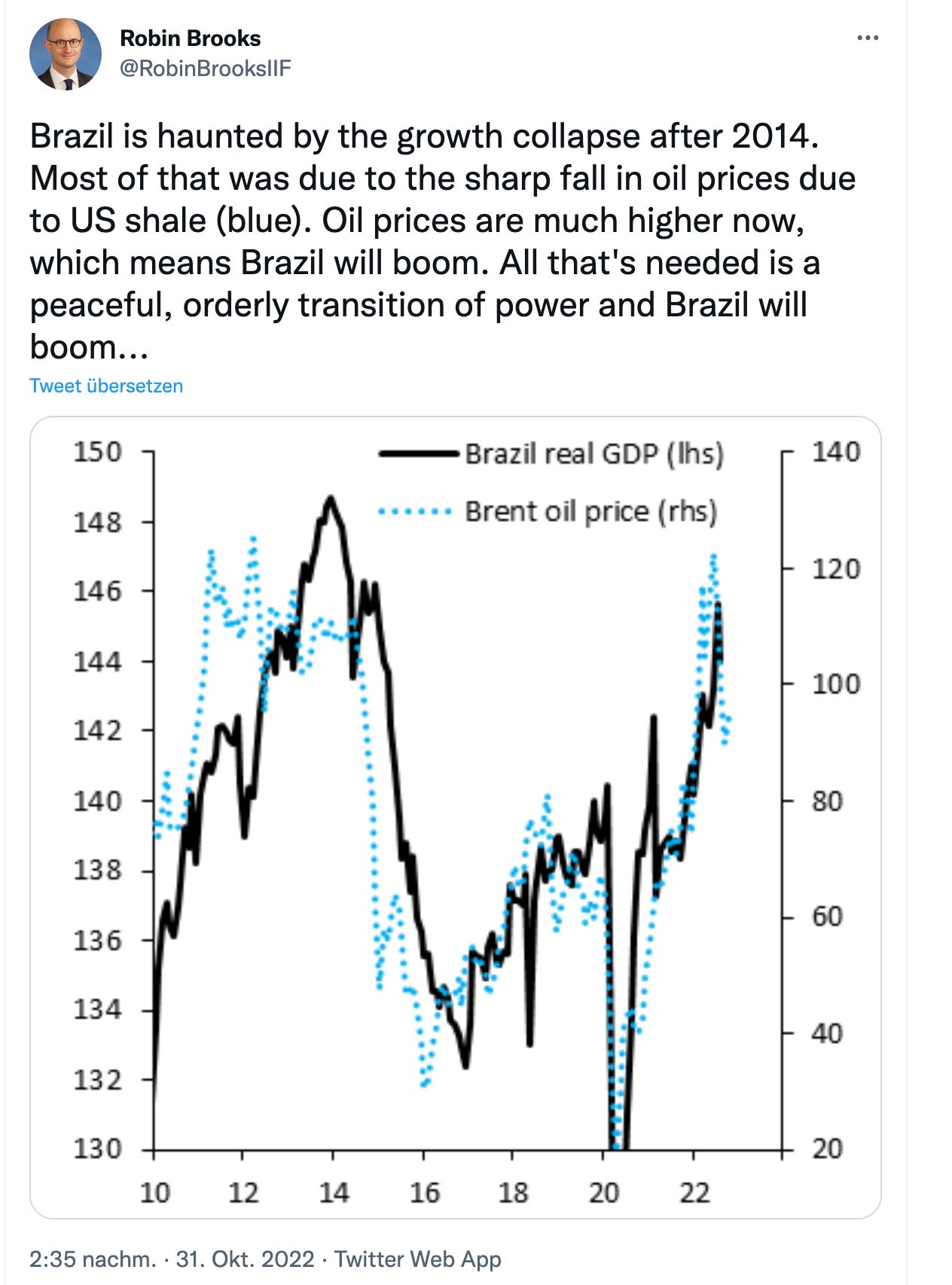

Brazil is one of the few countries that hiked interest rates early. As a result, the Brazilian Real has performed even better than the US Dollar this year. Its stock market doesn’t look too shabby — and the Brazil ETF currently yields 5.14%.

Lots of commentators are positive, like this guy:

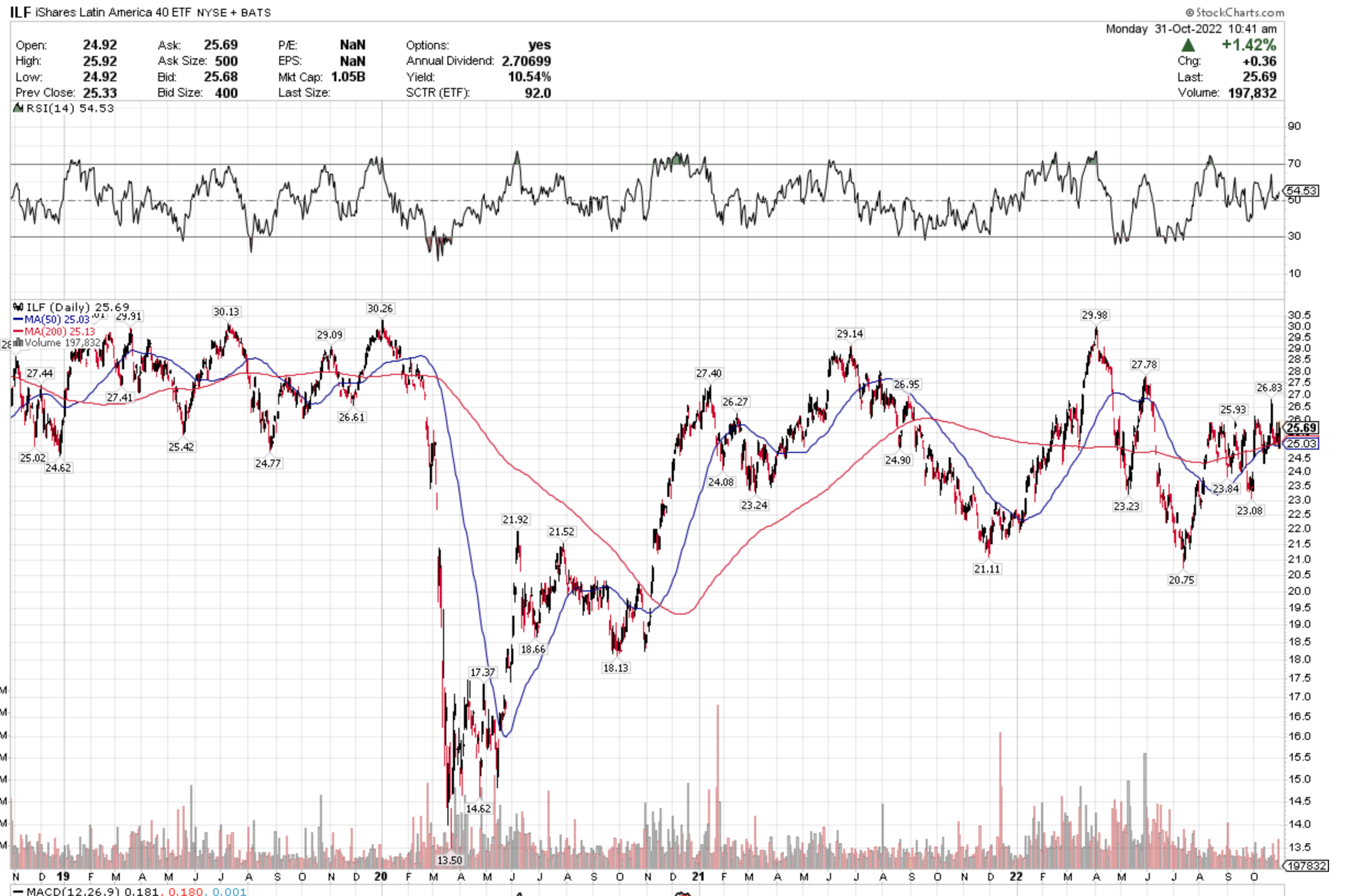

I recently considered buying the South America ETF ILF. The logic behind South America is similar to that of Brazil: they raised their interest rates a lot earlier than we in Europe/USA did; they are relatively unscathed by the Russo-Ukranian war; and they should benefit from what looks like a continued commodity bull market. To boot, ILF has a dividend of, wait for it, 10.54%!

However, taking a closer look, I discovered that its yield is over the place. I don’t mean like, they skip the dividend every six years or so, or they cut it by 30% at one point. No, it’s more like up 200% one year, down 50% the next, down another 50% the year after, then up again — so you really can’t count on it at all.

So, I find it difficult to buy ILF right now, but it will remain on my watch list!

Finally, Europe is already in a recession that will probably be quite severe. Stock markets typically turn positive before recessions end, so perhaps European equities present strong upside potential. Instead of waiting 6 to (worst case?) 18 months before you can invest in U.S. stocks, consider rotating from the U.S. to Europe. The relative performance of MSCI Poland may serve as a useful barometer of geopolitical risk, which could be a buy signal for the region.

Here, we see that Poland versus Europe may be in the process of bottoming:

If Poland vs Europe continued to develop in a positive manner, that would be a sign that the worst is over in Europe. And if you smash that “subscribe” button,

I’ll keep you posted!

Indeed, in terms of their yields, some European stocks might already be bargains. 8% dividends, anyone? My next article will highlight some of these, and discuss their pros and cons.

What’s your take on the stock market? Are you already dipping your toes into the waters? Please comment and let me know!

I think you're on to something, Martin. Investors in the US haven't really needed international diversification for over a decade, and many have probably given up on the idea -- which makes it the perfect time for the market to throw us a curveball.

A rising dollar creates headwinds for foreign investments. If I buy $1 worth of stock in a foreign company when its currency is at parity and then the US dollar rises 40% against that currency, the investment has to rise 40% in its local currency for me to break even.

If you splice together this US dollar index data series discontinued in 2019, https://fred.stlouisfed.org/series/TWEXB, with this newer one with less history, https://fred.stlouisfed.org/series/DTWEXBGS, you can see about a 40% rise from inception in the 1990s to 2002, then about a decade of decline, then about another decade of rise.

So if the past trends repeat and the US Fed stops raising rates, I'd anticipate a good decade ahead for an internationally diversified portfolio.

I look forward to your follow up article!