60/40 May Be Dead, but Other 'Lazy' Strategies Weren't So Bad in '22

60/40 May Be Dead, but Other 'Lazy' Strategies Weren't So Bad in '22

The jury is still out on whether the classic, “conservative” mix of 60% stocks and 40% treasuries is really dead.

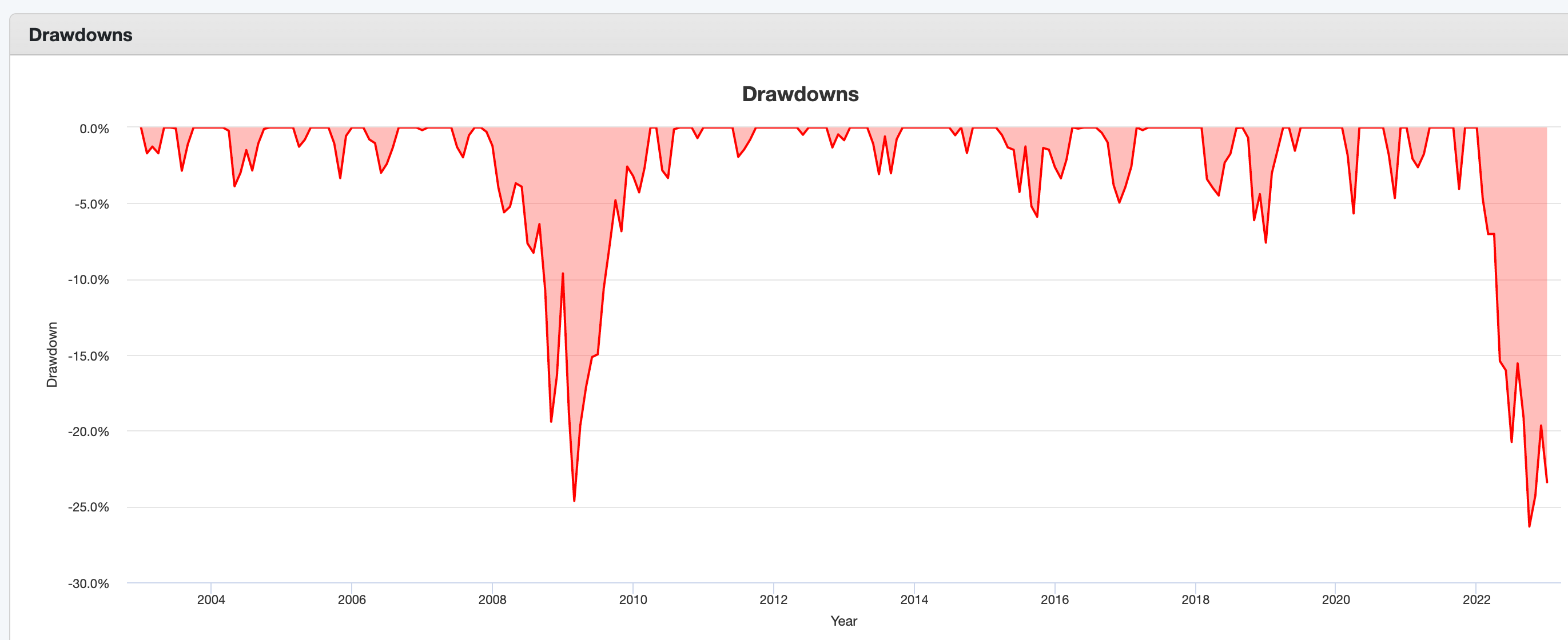

Some say, after 60% S&P 500 / 40% TLT lost an almost unprecedented 23.4% in 2022, the damage is done, and there is no danger of a re-occurrence. In terms of treasuries, the Fed rate went from 0.5% to 5% this year, but there is little chance of it advancing further from 5% to 9.5% — the opposite is more likely.

Those, like Michael Gayed, who say 2022 was an anomaly, posit that one doesn’t change a strategy because of an occurrence that has happened only one time in history:

Gayed may be right. On the other hand… 2008 was also an anomaly — real estate had never blown up like that before. Who could have known?

And so was the 2000 dot-com crash. Technology is important; it is the basis of modern capitalism. Tech stocks going down, in aggregate, 90%? Not really possible (in foresight).

We (try to) learn our lessons. We know that trees don’t grow into the sky, and that even real estate can’t keep on appreciating in value forever. We know that tech is important, but we watch its valuation because a bubble will tend to burst, sooner or later.

Are Gayed et al saying, the markets have their basic rules and principles, and these are not changing just because of one bad year?

Or is he saying, this horse won every darn race until now, and I’m not gonna stop betting on it just because of that one nasty stumble?

I’d argue: we have seen that always relying 100% on treasuries as your risk-off asset is foolish.

Inflation is back due to a number of reasons, such as: the expensive decarbonization of energy, and subsequent under-investment in petro capacity; populist de-globalization (so we’ll have less cheap products coming from China); demography (causing a tighter labor market)…

So, we need to expect occasional bouts of rising prices, which will then be fought by a newly vigilant Fed, which has (hopefully) learned its lesson from 2021.

As I have written in the past, you can still invest in treasuries when their moving averages have positive momentum. Treasuries are also comparatively safe when inflation expectations are low.

But please don’t permanently allocate your fortune into 60/40, hoping for the best, unless you don’t mind seeing this kind of result:

So, what can else you do (besides 60/40), if you wish to invest your money with a low turnover?

Firstly, Harry Browne’s Permanent Portfolio lost only 7.78% this year if your treasuries were of the mid-term, 3- to 10-year type (IEF). I wrote about this investing principle in May.

To recapitulate, it uses a quite simple recipe: invest in one-fourth cash, one-fourth gold, one-fourth stocks, and one-fourth treasuries. Once every year, you re-balance, to get back to this ratio.

Each of these assets work in different economic conditions. Stocks in good times, bonds in bad times, gold in inflationary times, and cash when everything is falling apart and nothing works.

While 2022 was inflationary, the gold hedge was a bit feeble, so I’d consider this a “nothing works” year. You might therefore think this year would be a negative outlier for the PP, which makes it all the more surprising it turned out comparatively OK.

The compound growth rate of the Permanent Portfolio since 2003: 6.24%; maximum monthly drawdown: -12.75%.

Using proxies since 1972, only seven years were negative: 1981, 1994, 2008, 2013, 2015, 2018, and 2022, the last year being by far the worst one. Here’s the link, should you want to replicate this data.

Second lazy strategy: Low Volatility

It is somewhat counter-intuitive that betting on low-volatility stocks is rather successful in the long run. No risk, no gain, right?

But actually, as Harry Long wrote a few years ago, in the stock market, it is more important to not lose a lot of money in the lean years, than it is to make a big amount of money in the fat. Few understand this.

Here’s the logic. Due to the nature of compounding gains and losses, a strategy that has low volatility has the possibility of beating the market across an entire bull/bear cycle.

For example, a 50% drawdown necessitates a 100% recovery in a portfolio to break even. Risk vs. return has a non-linear nature. You don’t get long-term outperformance by rising more than the broader market during strong up years. Instead, you outperform across a cycle by underperforming during strong up years and outperforming during strong down years.

Luckily, we don’t need to select a dozen or so low-volatility stocks to test this theory. We can use SPLV, the low-volatility ETF. Yearly-rebalanced 80% SPLV and 20% cash, since 2012, earned 9.03%, and lost only -3.54% in 2022.

If you employed mid-term treasuries instead of cash, your long-term gains would be slightly better, and your maximum drawdown would be somewhat better than the cash variant’s -17.15%. But your loss last year would have been -6.95% — also not too bad, but not as nice.

Note well that this strategy underperformed in 2020, the violent year when a waterfall crash was followed by Fed-induced stonkishness, losing -1.14%. It seems that low volatility means foregoing the gains that come from extreme swings. If you are interested in investing in SPLV, perhaps you’d consider allocating only a part of your capital to it.

The low-volatility approach takes moral fortitude to implement in the long term. When everything is booming, and the stock market is in bubble territory, and your next-door neighbor is bragging how he made double as much as you did by investing in Bitcoin, will you be able to smile and say great gains come with great risks?

So, please consider just buying and holding SPLV for a not-large percentage of your portfolio. That way, you reduce its total volatility — but you don’t get hit hard in years like 2020.

Currently, SPLV yields 2.9%, and has just recently gone into “Golden Cross” territory, after its 50-day moving average crossed over its 200-day moving average.

Another lazy strategy: Consumer Staples 60/40

The theory behind this one is: Even in bad times, people need to eat. So, arguably, a percentage of consumer staples stocks belong in every portfolio.

XLP/IEF (yes, I’m back with treasuries!) 60/40, yearly re-balanced, since 1999: CAGR 7.46%, maximum monthly drawdown -13.38%. Return 2022: -6.58%

Or combine Low-Volatility with Consumer Staples?

I’ve convinced you that treasuries are not necessarily an asset for all seasons, but you like the ETFs I’ve presented here? Then how about a mix of one-third cash, one-third Lo-Vol, and one-third Consumer Staples, rebalanced yearly?

Now, that’s a nice and steady equity curve. This year, it lost only 1.34%. (CAGR since 2012: 7.65%; maximum drawdown: -11.67%).

One final note: most of these approaches can be improved by re-balancing more often, or by adding moving averages. That means, you’d have to check these strategies every month, in some cases every day. But since this article is concerned with strategies that require your attention for only 15 minutes a year, that would be a story for another day…

By the way, I always appreciate any comment you might be willing to make!

Terrific article, Martin. Thank you for your continued work.

Nice ideas on "lessons learned" from 2022. I like your idea of both lower volatility, coupled with better returns, and the short survey of how to do both, benchmarked against 60/40.

Maybe point out the improved performance related to the "black Swans" you mentioned, tech bubble, real estate crash, etc. with a 60/40 benchmark overlay, or PV chart?