It's Pretty Darn Easy to Invest in Treasuries

It's Pretty Darn Easy to Invest in Treasuries

if you stop expecting miracles

As I am sure you have heard, this has been the worst year for investing in a traditional, they-told-you-so-prudent mix of 60% stocks and 40% government bonds in maybe 5,000 years.

SPY/TLT 60/40 for instance: -26.32% year-to-date (end-September); who would have predicted this? With mid-duration treasuries (IEF) or all-bonds (BND), you shave off 6% of the loss, but remember: we are talking about a year where you lost, in addition, close to 10% due to inflation. So this is really yuuge and horrific.

But I am here to tell you that this didn’t have to happen. If you really want to enjoy the often-low correlation to stocks that treasuries have, if you think they are a necessary element of grown-up investing, then you can reduce risk with a very simple and unsophisticated method.

Just apply (link here) the old, time-tested strategy of the Golden Cross/Death cross. Yes, the method that they say Japanese rice traders developed three hundred years ago. It means applying two moving averages to the price of your bonds: a 50-day, and a 200-day moving average. You buy your asset when the 50-dma crosses the 200 moving upwards; that’s the Golden Cross. The Death Cross is the sell-signal equivalent on the way down.

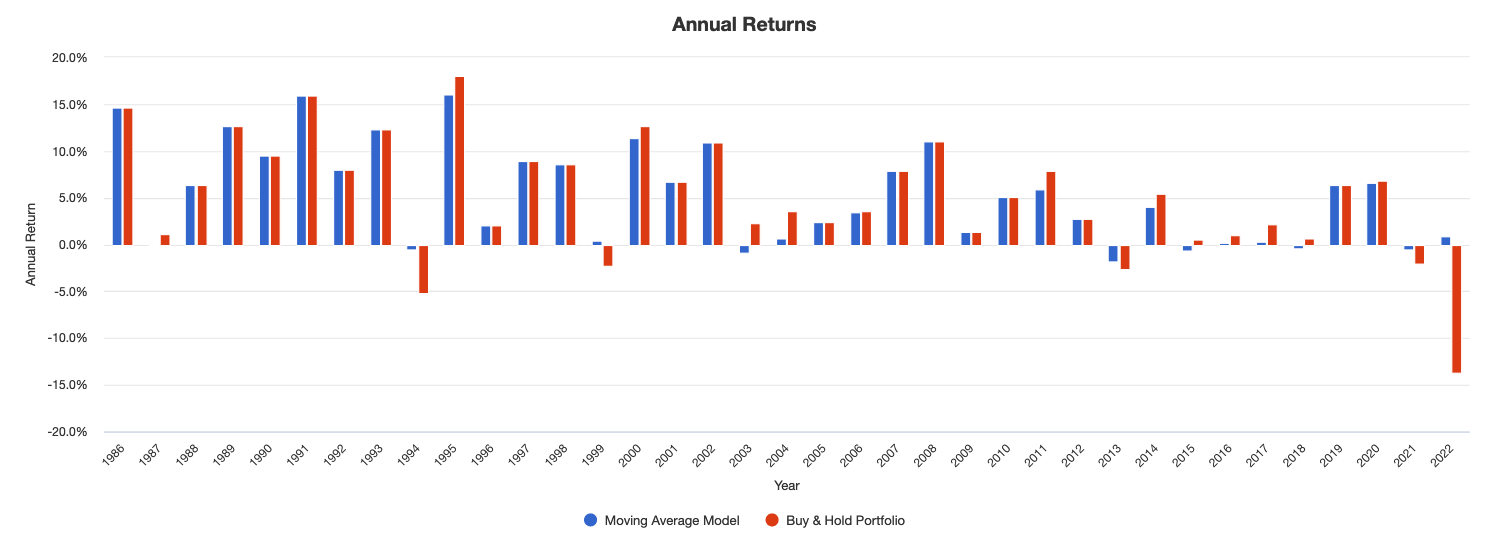

What we have then is a leisurely, lagging signal that still protects you from the worst drawdowns, and lets you sleep at night, with a growth rate (CAGR) of 5.27% from 1986 (using the Fidelity fund FGOVX), and a maximum monthly drawdown of only -5.68%.

In 35 years, only 6 ended negatively, with none worse than -1.82%.

Show me another easy-to-use strategy with a 35-year track record, with a MAR of almost 1, that went into cash 309 days ago before you poo-poo these results, please.

Yes, that going to cash 309 days ago, means it lost earned 0.84% this year, to end-September.

Agreed — returns were outsized in the inflation-reduction 1980s, and weren’t so hot in the 2010s, with a particularly unsatisfying stretch from 2015-2019. I’m not saying you should invest all your money in this one. But I am saying it can be a useful diversifier because it invests in a principally low-risk asset (US Treasuries) in a principally low-risk way (by selling when things are going to pot).

Also, who knows what awaits us when this current episode of inflation is over? I know a few very smart investment guys who are licking their lips in anticipation of juicy treasury returns. This might be the 1980’s again, or 2008.

Other investment implications

In its core, the Golden Cross is a simple risk-off signal, so you might consider using it to decide when it is safe to use Risk Parity. Enjoy the excellent risk-adjusted performance e.g. of a QLD/TMF (leveraged Nasdaq/treasuries) risk parity strategy as long as our indicator says FGOVX is nowhere near the Death Cross, but go to cash when it gets iffy. I haven’t tested this one yet, but I will, going forward.

What about 60/40?

Potentially, this can be OK, too. Applying the Golden/Death Cross rules to a 60/40% portfolio of FGOVX (Fidelity Government Bonds) and VFINX (Vanguard 500 Index Investor) did lose 1.9% this year, but its long-term performance is rather better than with bonds-only: since 1986, +8.13% with a maximum monthly drawdown of -17.9%, with only five years that ended in the red, none worse than -5.32%.

Mind you, the worst drawdowns happened during the flash crashes of 1987 and 2020. Both of which did not cause pain for very long; as the Golden Cross is a very lagging signal, it’s a feature and not a bug that such market turmoil is damaging. If you subtract these two episodes, the maximum drawdown is a very manageable -8.4%. So your risk-reward ratio doesn’t actually look too bad.

As acceptable all this is to me, Golden Cross-based strategies are not world-beating, and using them certainly won’t get Ray Dalio to hire you. But I believe their performance is better than 90% of what is out there. If your investment adviser does worse, fire them. Surely, an investment strategy that not only has been working for decades if not centuries, and also got through this year’s troubles pretty unscathed is worth considering.

Thanks for reading! What do you think? Is this approach to old-timey, too stale for you? And do you have an idea how to add leverage, to scale returns up a bit? Let me know in the comments, please.

And please subscribe to my channel, if you like my content. It makes a difference!