The Usefulness of Bonds Depends On This One Crucial Factor

The Usefulness of Bonds Depends On This One Crucial Factor

and this factor is actually close to saying "you can buy them once again"

Government bonds were wonderful… until 2022, when they got horrible

Under normal circumstances, bonds are wonderful part of any diversified portfolio: as they do not correlate with stocks, they work as a counterweight. When stocks go down, bonds go up… But in contrast to gold for instance, bonds are productive assets that earn a return.

But put strong emphasis on the word “normal” in the first sentence. As any bond investor has seen this year, under the distinctly “un-normal” circumstances when inflation rears its ugly head, bonds can be terrible investments.

In fact, a “healthy” mix of stocks and bonds, aka 60/40, this year performed worse than it has for decades, probably for generations. Leading to a weath destruction that is unparalleled in most investors’ lifetimes:

A drawdown of 60% of GDP: simply brutal.

In hindsight, it was simple: Bonds suffer in an inflationary environment. Everybody knew that, yet most folks were too late to sell. And honestly, who expected 2022 to be so extreme that it wold be the worst year for government bonds since the Civil War?

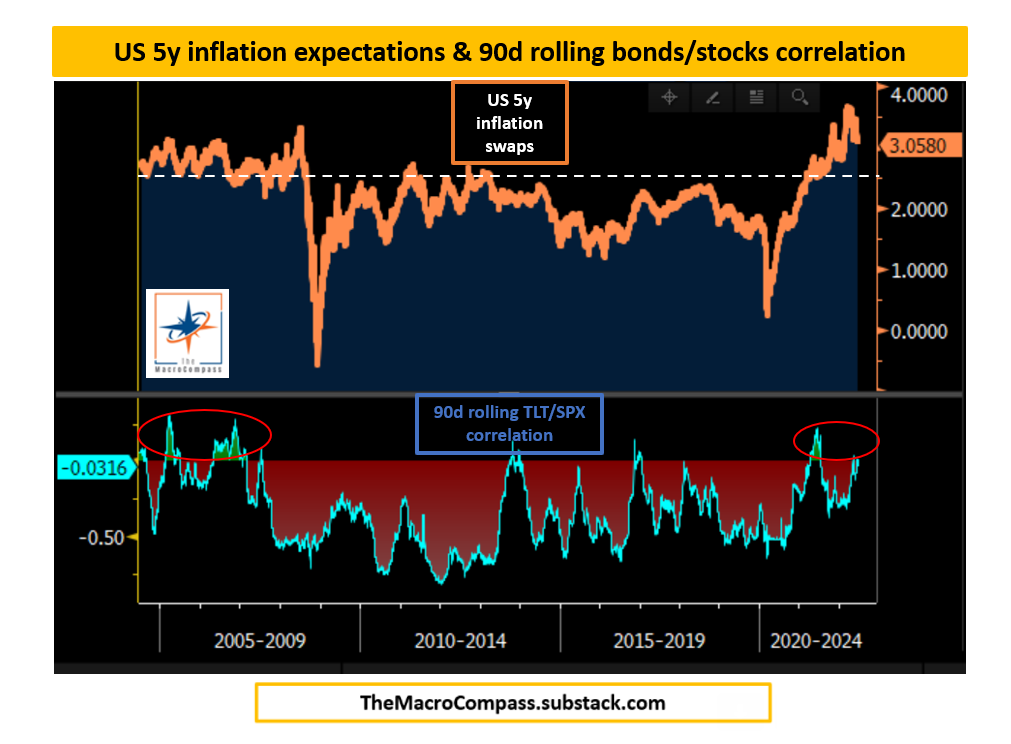

Cue to call MacroAlf, the former head of a $20 bn investment portfolio. He recently pointed out that there is a rather simple predictor of when the inverse correlation between stocks and bonds is no longer valid: when inflationary expectations rise above around 2.5%.

The following chart

shows a 20-year history for the US 5y inflation expectations (swaps, orange) against the 3-months rolling correlation between bonds and stocks returns (TLT vs SPX 90d rolling correlation, bottom part of the chart).

The interpretation is very clear: keep inflation expectations comfortably around/below the 2% area instead and bonds are going to be negatively correlated to stocks on a consistent basis.

Instead, once you cross the 2.5% threshold in 5y inflation expectations the negative correlation property quickly disappears.

In even simpler words: if you see an indication that inflation is trending towards the 2.5% mark, then no longer use bonds as a volatility-reducing hedge. Instead, use cash as your out-of-market asset, or some kind of split between cash and gold.

So, how can we use our new knowledge of the fragility of the stocks-bonds inverse relationship?

If you are a 60/40 investor, then I am sorry to tell you it seems adding a stop-loss is your only option. Doing this would have reduced your total losses this year to -8.79%, but comes at a considerable price to long-term performance, with CAGR since 1988 down by almost 2%. And the weird year 2015 would have ended up with negative 9%, much worse than buying and holding your 60/40 ratio (which would have gained +0.13%).

However, if you follow strategies that (until 2022, quite sensibly) used government bonds as their out-of-market asset, then my advice would be simple. Just use “cash” as the out-of-market asset as soon as inflationary expectations heat up!

For instance, this very simple strategy which buys or sells the closed-end fund PTY, about which I have written in the past, is greatly improved by going to cash in 2022 instead of sticking with the original long-term treasury TLT: -5.48% YTD, versus -18.0%.

I can’t see any major downsides to this. Most of the concerned years don’t suffer from using cash as your risk-off asset. But in general, I would be glad to pay an insurance premium if it helped prevent another 2022-style loss.

Where are we standing today?

Friday, July 1: according to the free FRED website, inflation expectations have recently plunged: down to 2.08% — hooray!

This is a snapshot however, and not an indication of a long-term trend. You might want to wait to see how the trend stabilizes before plunging back into buying treasuries. Or, it might be advisable to scale into buying TLT, starting with a nibble (as I am doing) and buying more every week as the trend becomes more clear.

Keep in mind, please, that we are only one really miserable inflation data point from yet another government bond bear market. We’re not in the safe zone yet!

Summing up:

Treasuries are great! But only in non-inflationary times. If there is a clear danger of inflation rising above 2.5%, then sell those suckers and go to cash, or to your other preferred out-of-market asset.

Terrific concept and post. I appreciate your ongoing work at ETF Algos!

Thanks for the kind words, Dartz! Much appreciated.

Please note the trigger level is 2.5%. 2 and under is comfort zone...

As to your other questions, I think Alf addresses several of them in his original post. In addition, NN Taleb, on his recent twitter feed, supplies a detailed mathematical analysis, if you're into that thing.

But this is just a quick reply from me, more to follow tomorrow.