A Few Quick Updates

A Few Quick Updates

Colombia, Philippines, and Zahorchak -- not in that order, though

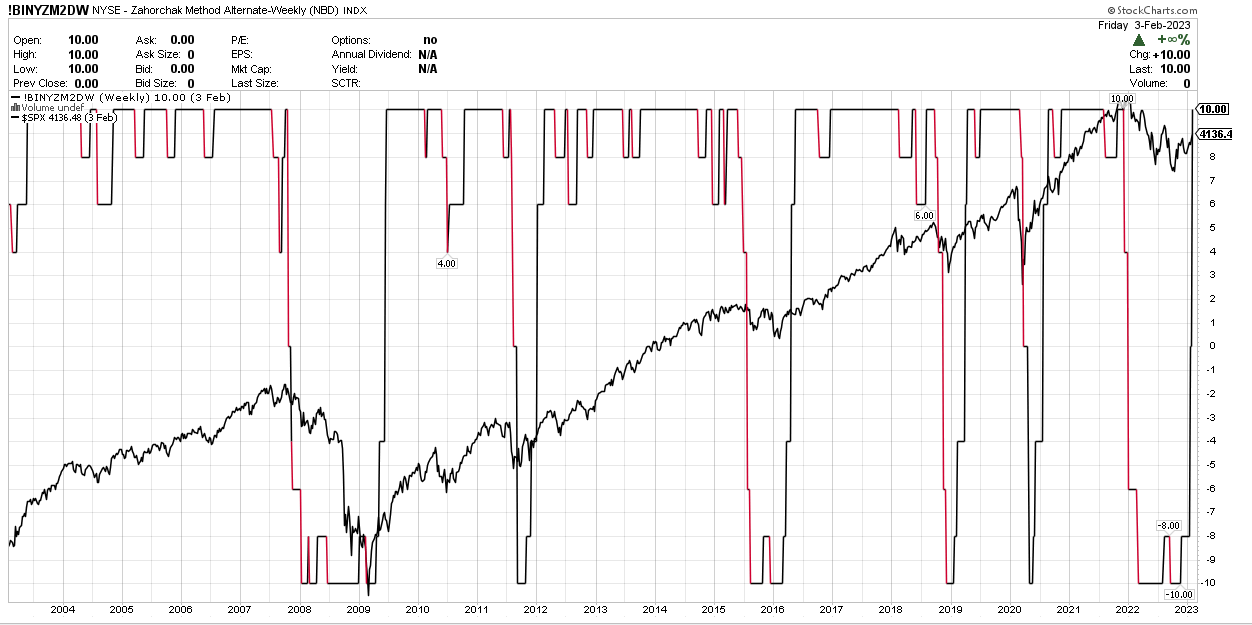

A few days ago, I said I expected the Zahorchak Indicator to power upwards to the “10” value, indicating a clear buy signal. Well, the other day, that is what happened.

Since 1980, this risk-on signal has been right in 12 instances, and wrong in one case: in 2000, when it advocated getting back into the market. It took over two years for it to correct this mistake.

To save you the effort of re-reading my original post: Zahorchak’s defenders say the Y2k incident was caused by the S&P500 having been at that time unduly influenced by large-cap tech — which went through an unprecedented bubble from 2000-2003.

If you take away big tech and look for example at MASKX, a small-cap fund, you see that the Zahorchak signals worked quite well — keeping you in the market until around May 2002, then signalling a “sell”; then getting you invested again in March 2003.

So far so fair, but that sounds like a perfect way to defend any signal. “You just needed to apply it to other assets”, is an after-the-fact explanation we’ve heard before.

Also, the 2000-2003 bear market apparently wasn’t characterized by the typical recessionary two back-to-back quarters of negative growth, so “that time, it was different”. Agreed… but it’s different almost every time.

Slightly worrisome: what if we in 2023 get another “atypical”, bear market like the one in Y2k, with no real recession, but mainly consisting of asset bubbles being burst?

Just my long-winded way of saying: don’t bet the farm that this very good signal performs perfectly this year.

Another way of investing based on the Country Mean Reversion approach

Yesterday on Twitter, Mebane Faber asked, “Forgot to update this at year-end...what asset classes or country stock markets were down three years in a row going into 2023?”, together with this table:

That was a face-palm moment for me. As I am sure you noticed, I recently posted a piece about investing in those countries that fared worst in the previous year or years. Yet, I didn’t think of investigating into what happens if a country was simply negative (but not horribly so) for two or three years in a row.

Long story short: I am buying some Colombia (GXG), and some Philippines (EPHE), because their stock markets performed negatively in 2020, 2021 and 2022.

(In January, GXG gained 6.45%, and EPHE 7.37%, so we are a bit late. However, if the average return of over 30% over the last 120 years is at all a yardstick, there are some more gains waiting to be gotten…)

Oh, and one more thing…

I recently bought some PTY. This post; this strategy.

Sorry for notifying you so late, I’ll try to be more timely in the future!

Addendum one day later:

Well, what about countries that were down not three, but down two years in a row? I mean, earning within a year +19.5% (on average) or +14.97% (mean) is nothing to sneeze at. So here you go: Korea, China, Malaysia, and Emerging Markets.

Some of these may have already worked out a little too well this year — here’s looking at you GXC, your 12.38% gain in January makes me feel a little stupid. Live and learn: my calendar now says I need to check this system again on January 1, 2024.

Please subscribe to my Substack, and I’ll let you know my picks for 2024, next time in a more timely fashion!