A quick year-end check: A speedy recovery remains unlikely

A quick year-end check: A speedy recovery remains unlikely

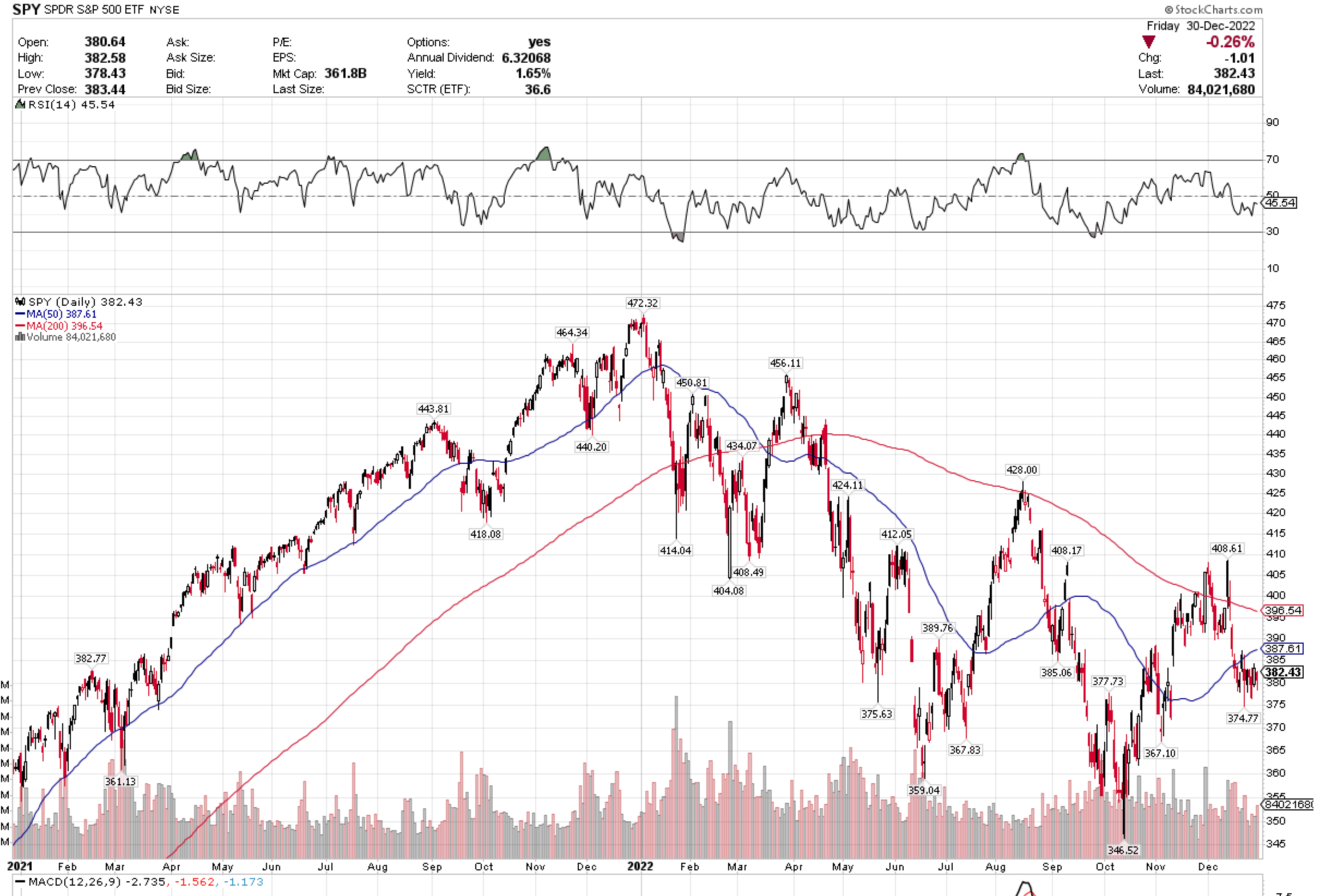

Happy New Year, everybody! Since I haven’t posted anything about the general state of the markets since October, let me just post a quick update on how far the present bear market has progressed, and whether we can hope to exit it soon.

There’s not much to like about the S&P 500. We may be getting closer to a Golden Cross, where the 50-day moving crosses above the 200-day moving average, but as long as the latter is sloping downwards, I wouldn’t consider this to be an actionable timing signal yet.

The consensus is for a recession in 2023. Looking at a weekly chart, we see that recessions are typically characterized by the S&P 500 plunging through the weekly 200-dma.

Currently, we’re nowhere near that area, so… beware! Lots more to lose if we actually do see a recession in ‘23.

Long-term sentiment readings, about which I first wrote in March 2022, may give some reason for optimism in the coming new year. Recently, sentiment (as measured by the ratio of puts to calls in the options market), has been at unprecedented negative levels. So, we are at the state where a new bull market would be in the realm of the possible: the 2020 turnaround happened around this level 0.69, as did the beginning of the new bull in 2012.

However, the 2016 bull started at an even higher ratio of negativity, and even more so for the GFC. For us to reach the level at which the 2009 bull began would take quite a few more months. I’ll let you know when the first signs of a turnaround appear.

In case you were going to ask, the Baltic Dry Index isn’t displaying anything I like, either.

What about the China wild card?

So, all of this points toward a classic economic-cycle theater play: In its quest to kill off inflation, the Fed will cause unemployment to rise to non-trivial levels. Companies will suffer from lower profits, thus compressing P/E ratios. This has the potential to create losses for the S&P 500 of an additional 20-30%.

But what about China’s opening up after many months of Covid lockdowns? This could be quite positive. Re-activated industrial activity could remove all the remaining supply-capacity restraints which were so inflationary in 2020-2022. And a spending spree by Chinese consumers could be a positive for all kinds of segments, such as consumer durables, or travel.

On the other hand, a resurgent China could be globally inflationary: post-lockdown countries consume more energy and foodstuffs, for instance.

What will the sum effect be? I really don’t know. But in case the news from China is unexpectedly positive, we might get a “soft landing” after all, so please be prepared.

What is your game plan for 2023? Comment and let me know, please.

And have a healthy, happy, financially successful new year!